The internet and technology over the past couple of decades have seen Credit Unions transform drastically. All for the better! One of the most impactful changes is the ability to make smarter decisions through the use of "Big Data" and insights.

More data was created between 2013-2015 than in the entire previous history of the human race!

Not only that, but data is growing faster than ever before and this year, around 1.7 megabytes of new information will be created every second for every human being on the planet.

When it comes to performing credit checks in Credit Unions, there are plans on the horizon to make the automation of your CCR enquiries even more efficient.

Data-driven decisions in Credit Unions.

Now

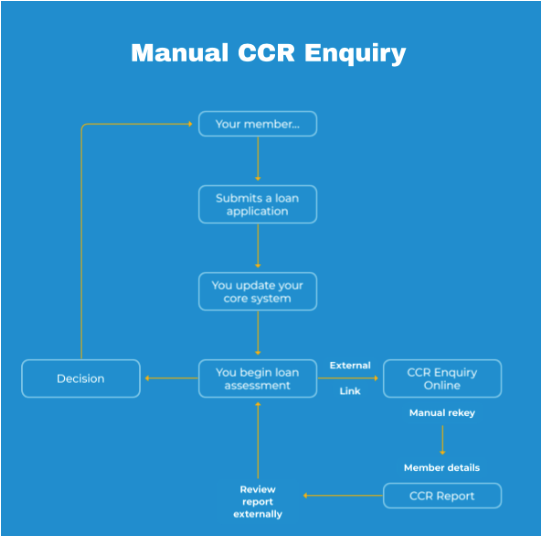

Currently some Credit Unions perform CCR enquiries manually. The below image shows a manual CCR enquiry.

As you can see from the diagram, a manual CCR enquiry requires the member of staff to access an external link (the CCR Web Portal) outside of their core system, meaning all of the member’s details need to be rekeyed, which takes more time and there’s more room for human error.

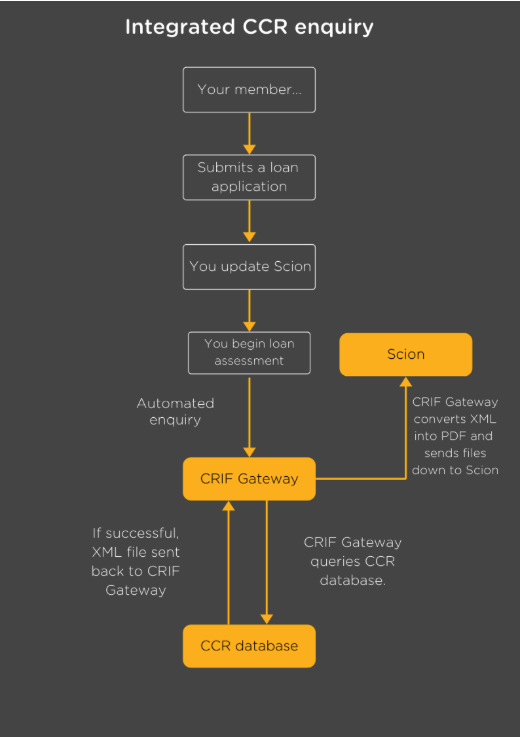

Below shows a diagram explaining the automated CCR enquiry process.

Some Credit Unions use Wellington’s integration with CRIF for integrated CCR enquiries. This integration with CRIF means that the entire CCR interaction occurs solely within your core system and requires minimal manual intervention. The data from CRIF is automatically stored in your core system, meaning no manual rekeying of information. This saves time and improves accuracy.

Because the information is automatically stored, it means your core system always holds the most accurate, CCR report data. You don’t need to worry about delays in staff rekeying information, or any human errors that have occurred.

Credit Unions now have an option to gather information from both the CCR and ICB, and be sent a de-duplicated report. This gathers information from both sources, and combines them into one, easy-to-understand report, meaning Credit Union staff don't need to read both and pull the relevant information from two reports. This saves Credit Unions valuable time, and drastically reduces inaccuracies.

(Near) Future

CRIF make use of the data sources available to them - one being CCR - and this bring around many other opportunities. One of which is recommended decisions.

Scion currently does this, by scoring members based on criteria such as loan repayments, money saved in Credit Union account etc.

The CCR will not replace the existing credit bureau (ICB). Actually, CCR and ICB are set to become complementary to one another. It will take time for the CCR to build up a credit history equivalent to the ICB and certain types of credit will be exclusively held in either one or the other database.

So by combining the Scion score with the information from ICB, CCR and Visonnet along with the preconfigured CRIF decision engine, the system can produce a more accurate recommended decision for a specific loan application.

This will give Credit Unions more confidence in loan decision-making and vastly reduce the time taken to make the assessment, and pave the way for the future of a full decision-as-a-service (Daas).

Decision-as-a-Service

The better quality data your system holds now will benefit your Credit Union in the near future.

DaaS is just around the corner and if your system stores good quality and up-to-date data, it will eventually be able to generate automatic decisions based on preconfigured rules and past occurrences that will virtually eliminate any manual intervention in your loans process.

This will give you more time back to strategically promote your services to members, with your core system doing all the heavy-lifting when it comes to providing loans.

Talk to us today about our new, enhanced loans module!